M&G plc: Go with the flow

[All company statements, images and transcripts are taken from the “Investors” section of the company website: https://www.mandg.com/investors]

In my last post on M&G plc I discussed three of its 2025 targets and the potential for their realisation. I suggested that M&G’s reputational standing might be better served with a more sober communication about the targets it can realistically attain.

With this short article, by the way, I want to attain nothing else than entertainment. This is no stock picking advice in any shape or form, neither long nor short. So here we go.

And in getting going, we understand that there’s no way around it: increasing assets under management (AUM) is the only way for M&G to reach its highly ambitious set of 2025 goals. As I’m talking here about a company that can be principally described as an asset manager, this assertion is not much of an insight.

Still, I would argue that flows – the money that goes into and leaves the asset manager – are more important than the total amount of AUM, because AUM go up when the market goes up, and down when the market goes down. Tracking AUM relative to market movements displays how well the capital allocation strategies of the asset manager work, but only inform tangentially about clients’ perception of the investment proposition of the asset manager. Clearly, in the long run an asset manager that underperforms the market will see client money outflows, but there is no strict correlation, as clients might be satisfied with a less stellar performance if the strategy of the asset manager offers them better prospects for both capital preservation and long-term appreciation than the volatile markets. Hence, client money flows appear to be more important than AUM for projecting the future success of an asset manager like M&G.

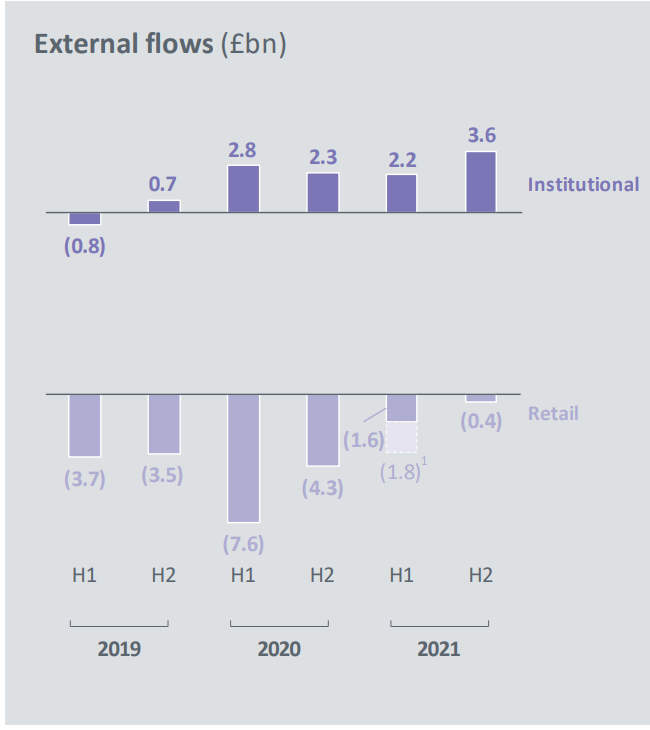

In preceding years, M&G suffered retail outflows, but saw resilient institutional money flows (from the FY 2021 presentation):

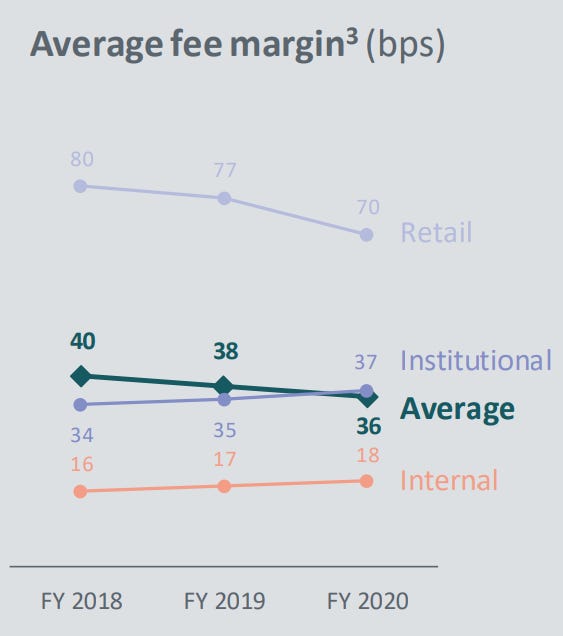

The retail outflows may be explained by unsatisfactory performance coupled with high fees relative to low-cost investing propositions like index ETFs. M&G reacted to the retail outflows with hiring new talent to improve investment performance, reassessing investment strategies, and progressively reducing prices. As to the latter point, here are the fee margins up to FY 2020 (from the FY 2020 presentation):

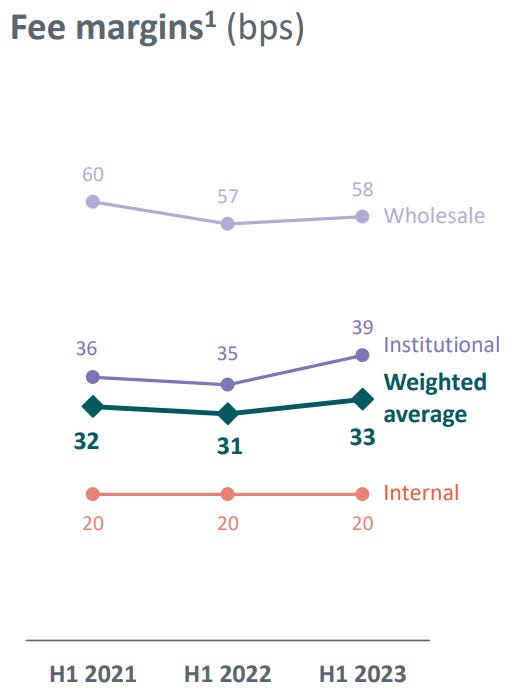

And here the margins as of last reporting, H1 2023 (I also included this graphic in my last article, from the H1 2023 presentation):

In order to stem retail/wholesale outflows, M&G had to drop the price of its product offering. Its average fee margin fell from 80 bps in FY 2018 to 58 bps in H1 2023. What stands out, however, is the uptrend of the fee margin in institutional asset management, which moved from 34 bps in 2018 to 39 bps in H1 2023.

This observation ties in with what I wrote in my preceding blog post: M&G has little flexibility to reach its 2025 targets with increasing margins, because meaningfully increasing margins would mean increasing prices, which would trigger client outflows. As institutional asset management drove client money inflows in preceding years and also could keep its margin up, continued strong institutional inflow is of vital importance for M&G to prosper in general, and reach its 2025 targets specifically.

With this in mind, let’s take a look at how M&G’s flows fared in the H2 2022 “mini budget” crisis.

Putting institutional flows to the test (Or: The mini-budget crisis)

This crisis was set off in September 2022 in the UK when then-Chancellor Kwasi Kwarteng announced a mini-budget that included £45 bn of unfunded tax cuts. The announcement led to several days of turmoil in the markets and nearly spelled disaster for UK pension funds. The price of UK government bonds, called ‘gilts’, collapsed, as the cost of UK government borrowing increased and the value of the pound fell. The collapse in gilt prices caused a liquidity crisis for a specific kind of pension fund, Liability Driven Investment (LDI). LDIs are largely leveraged funds: they frequently use gilts as collateral to raise cash and buy more gilts. When the value of this collateral (the gilts) collapsed, the funds had to find cash either to repay the money they had borrowed or pledge more collateral. This need for cash forced them to sell gilts, driving down further the prices of gilts in the market, which in turn forced them to sell more and so on.

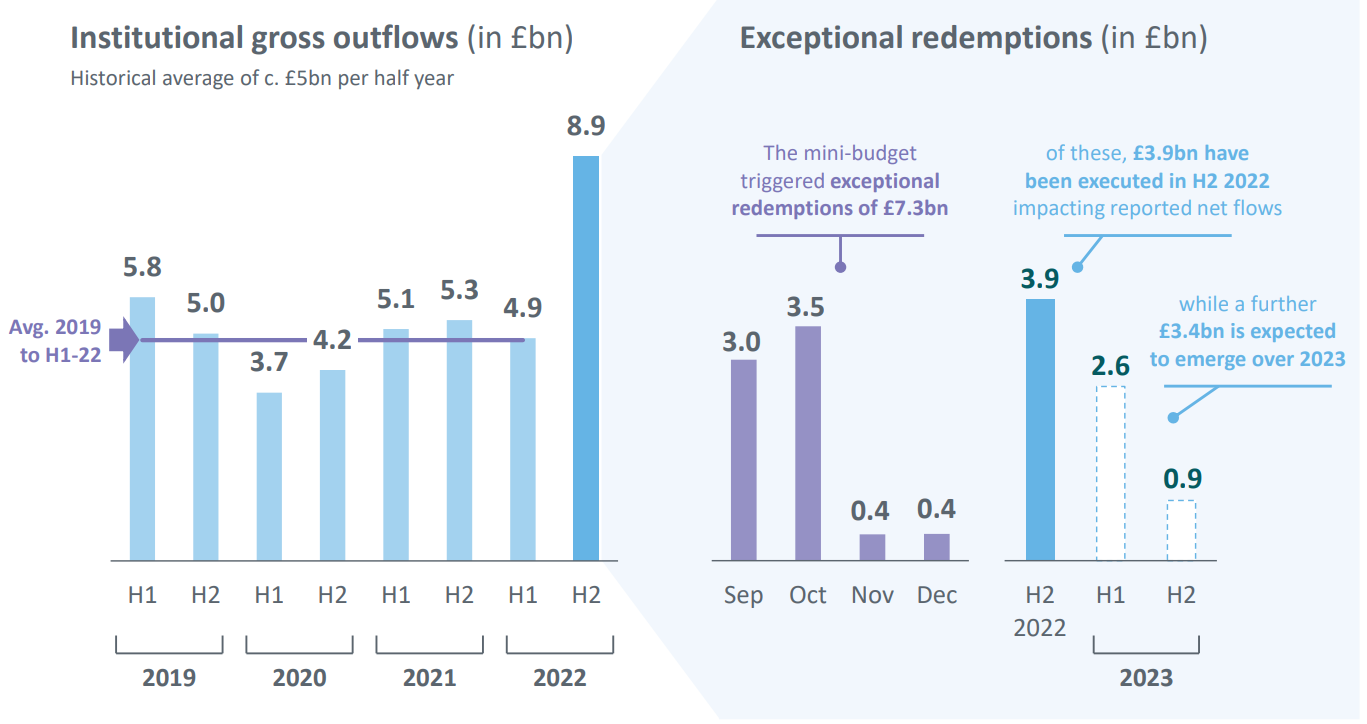

Consequently, either enmeshed in the turmoil or wary of it, in H2 2022 institutional funds withdrew double the cash from the M&G asset manager than they habitually do in a half-year period, resulting in net outflows of £0,7 bn for FY 2022. From the FY 2022 presentation:

As can be seen on the right side of the graphic above, M&G projected £2.6 billion of further gross outflows from the UK asset manager in H1 2023 as a lasting repercussion of the mini budget crisis. This was overly optimistic, and the final result was: “ … a tough external environment and headwinds in our Institutional franchise, where we saw £3.8 billion of net outflows here in the UK” (CFO, H1 2023 earnings call). With £3.8 billion net outflows, gross outflows will have been even higher if there were some gross inflows. Hence, it appears M&G significantly underestimated the aftermath of the mini-budget crisis and its corresponding UK institutional fund outflows. We might be inclined to believe that the further £0.9 billion gross outflows thad had been projected for H2 2023 won’t have captured the whole extent of redemptions either, although management so far has only talked about ‘some pressure’: “Well, I think if you compare to the first half, where you had significant outflows from the pension funds, we will still see some pressure in the second half” (CEO, H1 2023 earnings call). At any rate, the H1 2023 report is inaccurate: “Despite these expected redemptions in the UK, we have continued to expand our presence in Europe” – inaccurate, because of gross redemptions only £2.6 bn was expected, and not the £3.8 bn or anything north of £3.8 bn that actually transpired. In light of the failed projection for UK institutional outflows following the mini-budget crisis, one could possibly infer that management was either willfully too optimistic, or was in the dark about their institutional clients’ upcoming investment moves; both inferences wouldn't be ideal from a shareholder’s perspective.

Nevertheless, flows demonstrated resilience as the suffering UK institutional franchise was bailed out to some extent by the international institutional business: “These outflows were matched by strong growth with international Institutional clients, as we gathered £2.4 billion of net inflows” (CFO, H1 2023 earnings call). Hence, outflows from institutional asset management, both UK and international, were £1.4 bn in H1 2023, notably less dire than the £3.8 bn of UK outflows alone.

Moreover, thanks to positive flows to the wholesale asset management and wealth management, in total for M&G net flows were positive by £0.7 billion (from the H1 2023 presentation):

M&G underestimated the extent to which the mini-budget crisis would trigger pension funds to redeem their positions. Still, the asset manager was able to arrive at net inflows in both FY 2022 and H1 2023, and this time thanks to the segment that had been a drag on flows in preceding years: retail/wholesale.

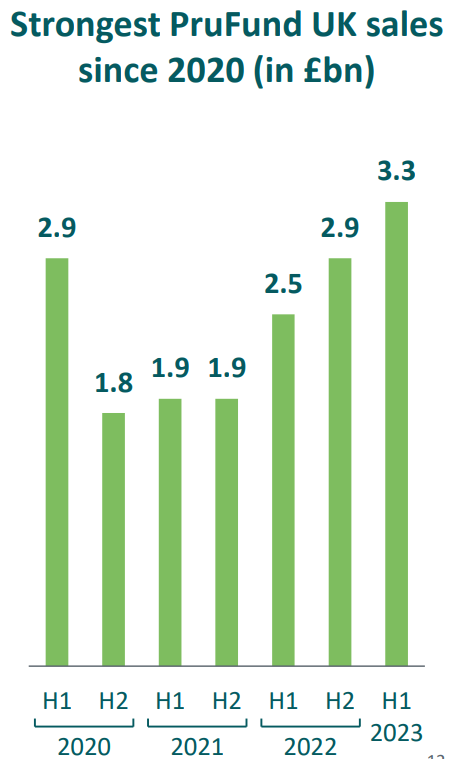

Here, volatile markets probably played into the hands of M&G’s most important product in capitallight business, PruFund, whose working mechanism is to smooth out up- and downturns and thus provide steadier returns for clients:

This graphic may indicate that PruFund is more appealing to clients in times not characterised by an equity bull market: PruFund sales dropped during the Everything Bubble lasting from H2 2020 to H2 2021. Management seems to confirm this correlation: “Its [PruFund’s] smoothing mechanism and diversified asset allocation are very attractive for clients, particularly in light of the ongoing market volatility we are seeing” (CFO, H1 2023 earnings call). Given that Everything Bubbles fueled by massive monetary stimulus are the exception rather than the rule, management understandably has a constructive view on the ongoing success of the PruFund proposition.

Conclusion

Shareholders might want to place particular focus on net inflows in their assessment of M&G’s progress in working towards its 2025 goals. It will be interesting to see if M&G manages both to revert the course of institutional outflows and bring them back to the former track record of inflows, and at the same time manages to keep up retail inflows by continually strengthening the PruFund proposition with clients. The latter point entails sharing an updated and more granular plan for scaling PruFund Europe, also called Future+, on which M&G’s management seems to have preferred keeping silent in the last reporting.