M&G plc: We promise you the moon

M&G plc: We promise you the moon

M&G plc is a UK based, but internationally operating company whose roots in the insurance business can be traced back to 1848. These days, M&G combines asset management with insurance expertise and offers a wide range of insurance, saving and investment solutions. The company has about 5 million retail clients and more than 800 institutional clients in 26 markets.

While M&G also offers investment advice to their clients, this article, to be clear, offers absolutely none, neither long nor short. It is written with the sole purpose of entertainment.

M&G was spun off from Prudential plc in 2019 and listed on the London Stock Exchange. Prudential actually spun it off because they wanted to focus on a more growth-oriented business model and M&G didn’t seem to fit into that proposition. However, now as a standalone company, it is growth that M&G pursues, and growth is the stated mission of the new CEO Andrea Rossi who took over in October 2022 and before had been the very successful CEO of AXA Investment Managers.

Since 2020, M&G has righted the ship of the wholesale asset management part of the business. Mr. Rossi looked back on this achievement of the company on the H1 2023 earnings call: “[I]in 2020 only 20% of our mutual funds performed above median, and we suffered net outflows of almost £12 billion. We believed that this franchise could return to profitable growth. So, we brought in fresh talent, tackled performance, and reviewed our proposition and pricing structure. As of the end of June, over 70% of our mutual funds performed above median, and we achieved positive net flows of £1.3 billion.”

While all the credit belongs to M&G for this feat, management’s 2025 goals might appear overly ambitious, at least in part. In this article I will take a closer look at three of their targets for 2025 and describe why they might overreach with two of them, beyond what will be possible within that time-frame. Overreaching in setting targets, and then failing to meet them, is not to be taken lightly: with shareholders, it could corrode trust in management.

The three targets I will discuss are:

“– Reduce core Asset Manager cost to income ratio to sustainably lower than 70%;

– Deliver increased adjusted operating profit from Asset Management and Wealth to more than 50% of the Group total, excluding Corporate Centre ; and

– Reduce our leverage ratio to below 30%” (H1 2023 report).

I will start with the last target, the one I think will probably be realised.

The debt reduction goal

M&G pursues deleveraging. What is reproduced above from the H1 2023 presentation is, notably, a debt call date profile, not a debt maturity profile. M&G plans to pay back the £300 Mio bond that becomes callable in 2024, but it will only come due in 2049. Hence, M&G implements a strategy of proactive debt reduction.

The bond callable next, in 2028, will mature in 2048. Without a doubt, shareholders should view and will view favourably when the company redeems the bonds as they become callable, instead of paying them off at maturity or rolling them over at maturity. With the redemption before maturity, the total interest expense is reduced on an advanced schedule; to date, the average interest rate M&G has to pay on its debt is 5,7%.

The goal is to bring the nominal value of the debt down to 30% of Own Funds by 2025. One further step for M&G to reach this target, beyond redeeming the £300 Mio bond, would be to increase Own Funds. The matter is addressed by CFO Kathryn McLeland on the H1 2023 earnings call: “[W]e do have a bond Tier 2 sub-debt that is callable in just 10 months of £300 million … [C]learly that would reduce our leverage ratio halfway towards the 30%. We can all figure out the maths in terms of what our own funds would need to do for us to get naturally to the 30% target by 2025.”

Still, Mrs. McLeland takes into account that M&G might not be able to sufficiently increase Own Funds: “So, we are confident in our own funds position … However, if own funds does not move, we would need to do more than the £300 million to hit the target” (H1 2023 earnings call).

What does the ‘more’ consist of? M&G could buy back bonds from holders in the open market, before their callable date. Mrs. McLeland indicates as much on the FY 2022 earnings call: “And the bonds are still trading below par, some of them 7/8%, but we are not in a rush at all. This is something we are going to be very thoughtful about. This is an important metric for us to reduce our leverage, we have got the callable bond next year. And over time, there is no change in own funds, we would need to go beyond the £300 million.”

With ‘cash and cash equivalents’ of £4743 Mio on the balance sheet at the end of H1 2023, M&G has the ability to redeem the 2024 bond and further buy back debt on the open market.

Hence, Mrs. McLeland’s conviction that M&G will reach the 30% leverage target even if Own Funds don’t increase, is readily explainable.

Nevertheless, this is the only goal of the three listed in the introduction to this article the realisation of which is strictly envisionable. With the other two, realisation is much more uncertain.

The cost/income ratio goal

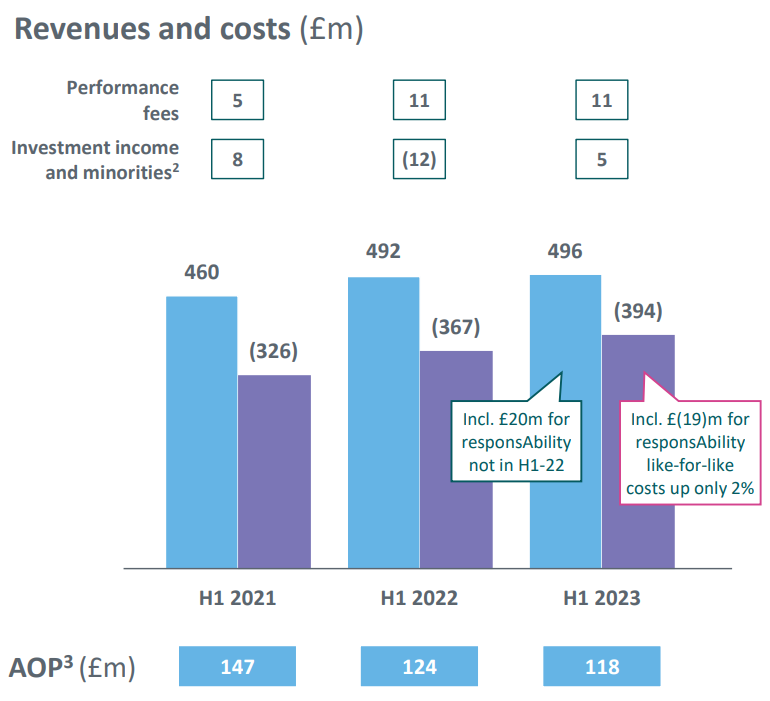

The goal is to bring the cost/income ratio of the asset manager down to 70%. Incidentally, as of H1 2023, the cost/income ratio did not improve, but actually declined sequentially, as can be seen in this graphic of the H1 2023 presentation:

The reference to the new fund responsAbility can be ignored here, because what responsAbility takes away from costs in order to have a like-for-like comparison y/y, it also takes away from additional revenue for H1 2023 – its effect on both revenue and costs equals out. So here is what the graphic means: the cost/income ratio in H1 2023 stood at its worst for the past three years. “The impact on revenue, partly mitigated by better margins, and the increased cost has resulted in an increase to the cost/income ratio for the Asset Management business to 79% (30 June 2022: 75%)” (H1 2023 report).

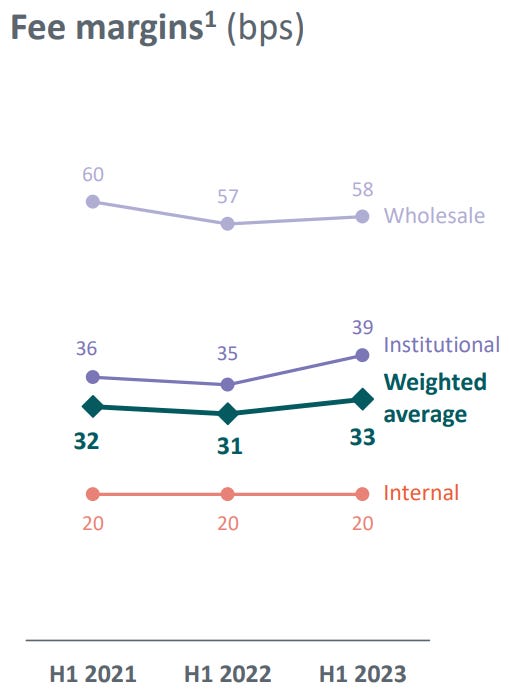

As stated in this quote, margins improved:

But as can be seen, margins are rather range-bound; it’s not that M&G could knock the lights out with margins. Increasing margins in a strong way would mean increasing prices, and hence risking losing clients to the competition. Mr. Rossi might have hinted at this hard fact when saying: “I mean, when you have that sort of investment performance with 44 of our funds in the upper quartile, I am not saying you should charge more, but I mean, I think when we check versus others, we are where we are” (H1 2023 earnings call).

Although there was no improvement, but a deterioration of the cost/income ratio over the last three years, Mrs. McLeland reiterated: “[W]e remain fully committed to our Cost to Income ratio target of below 70% by 2025” (H1 2023 earnings call).

Given the recent track record of the cost/income ratio, I consider this to be a highly ambitious goal which evidently would be great to see realised, but which seeing realised I wouldn’t consider a base case, but rather a slightly aggressive bull case.

The 50% capital-light target

In the H1 2023 presentation, M&G reaffirms the goal of 50% of operating profits coming from the capital-light business by 2025: from asset and wealth management versus from the more capital-intensive Heritage business. The latter comprises individual and corporate pensions, annuities, life, savings and investment products. It’s called ‘Heritage’ because it’s a business segment that is running off, as the majority of the products are closed to new clients.

Management fully recognises the profit generator that Heritage represents for M&G: “Our Heritage business is the largest one of them [of the three business segments Asset Management, Wealth and Heritage], and with its permanent capital and long-term investment horizon, supports much of our product innovation. The resilience of the cashflows from the back book is critical” (CEO, FY 2022 earnings call).

Apparently management views the profit stream coming from Heritage as so important that they decided to open up Heritage to new business: “First of all, I explained why we re-entered, and we reentered because the market became larger” (CEO, H1 2023 earnings call). It makes sense that, to keep that reliable profit source, the strategy of focusing on capital-light business (asset and wealth management) has to be tweaked somewhat, allowing for a continuance of the capital-intensive business (Heritage): “And we always said that we wanted to utilise this opportunity to top-up the natural run-off we had … It is going to be very selective, and it is really not to go beyond the natural run-off that we have” (CEO, H1 2023 earnings call). Management does not want to grow the Heritage business, but is now determined to stall the run-off of its existing book by opening Heritage up to new business in the DB de-risking market, in which companies and organisations either unload their pension schemes to insurance companies like M&G, or let them manage them.

A decline in Heritage shall be stalled, but the overall strategy of promoting capital-light business remains intact: “Ideally, I want capital-light growth. Asset Management is at the centre, Wealth management also … So, it will be contrary to what we said go heavy on capital heavy business and increase that even further.” The capital-intensive Heritage won’t be increased beyond its run-off.

Mr. Rossi highlighted M&G’s focus on profitable growth, but also the benefits of its integrated business model. And management asserted to be very selective in writing new business in Heritage, eschewing many possible deals to focus on those with highest return on capital for the company and where M&G could provide specific value to clients: “We will only consider those opportunities where client needs precisely match our capabilities. For instance, when a DB scheme is over allocated to Private Assets, an area we know very well” (CEO, FY 2022 earnings call).

As has been said above, in the H1 2023 earnings presentation M&G affirmed the goal of 50% of operating profit coming from the capital light business by 2025. An analyst on the earnings call, Nasib Ahmed, appeared to put a question mark to that target – because with writing new Heritage business, M&G would also need to further increase their Asset management and Wealth business to proportionately adjust for the increase in Heritage. The answer by Luca Gagliardi, M&G’s head of investor relations, could indicate that the 50% target will be lowered going forward: “I will just take again the first one on the 50%. Clearly, there is a business planning process that M&G goes through and is in the second half of the year … So, I guess what we are trying to say is we kept it [the target] here for now because we are still committed to that type of effort at full year when there is going to be a revised business plan” (H1 2023 earnings call).

The 50% capital-light target is so difficult to maintain because M&G is reliant on the capital-intensive Heritage, and reliant on writing new Heritage business to keep the reliant profits coming, but this new Heritage business at the same time pushes out incrementally their target for an equal proportion of operating profits coming from the capital-light business.

The goal for private assets

This target will be discussed here because it fully runs parallel to the 50% capital-light target, as private assets are the main profit driver of the asset manager: “While accounting for under a quarter of the Asset Manager AUM, our Private Market operations generate over 40% of the revenues, at a strong average fee of 55 bps” (H1 2023 earnings call).

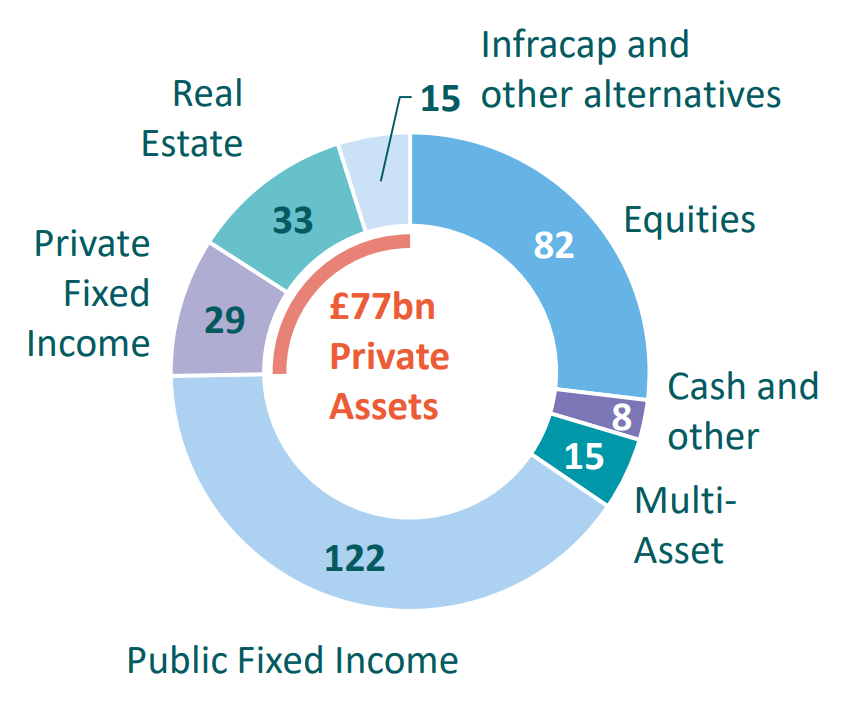

The following graphic shows the part of private assets in assets under management at the end of 2022:

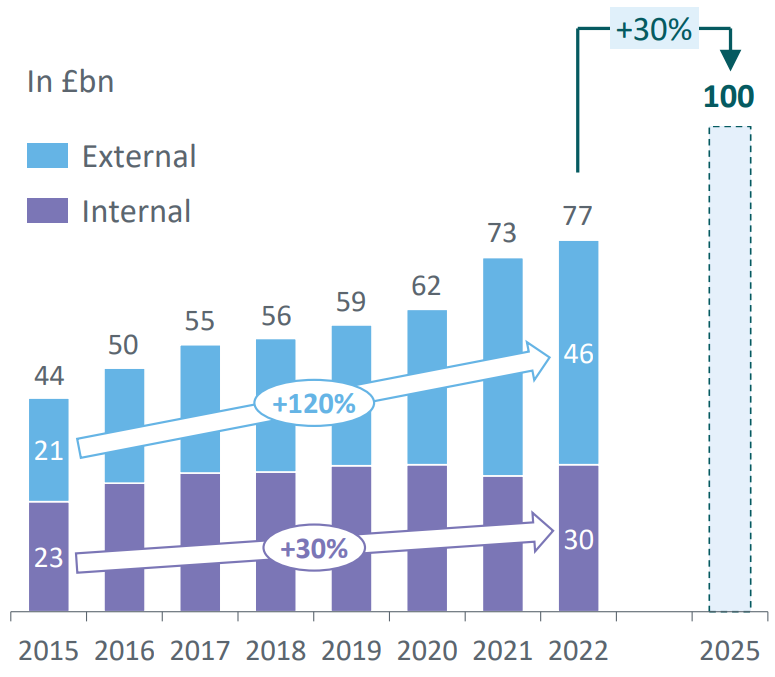

In the FY 2022 presentation, management gave its projection for the growth in private assets:

For this goal to be reached, obviously a meaningful growth is needed in 2023, 2024 and 2025. We have the first part of 2023 to look at so far. How have private assets fared? According to the Mrs. McLeLand, private assets helped drive the slight improvement of margins that has been mentioned before in this article:

“Our overall average margin is up to 33 bps, thanks to our continued efforts to expand the Private Markets business” (H1 2023 earnings call).

However, private assets actually declined: “Our private assets under management decreased to £73.8 billion of AUMA as at 30 June 2023 (31 December 2022: £76.6 billion) owing to negative market and other movements which more than offset £0.7 billion net inflows” (H1 2023 report).

Unless there is still a dramatic upswing in private assets in the remainder of 2023, the next two years would need to see unparalleled growth rates for private assets to reach £100 billion by year-end 2025. In this regard, it is a highly ambitious goal and, to put it mildly, I wouldn’t bet on its coming to fruition.

While a growth so unprecedented as to attain £100 billion in private assets by 2025 appears to be basically out of reach as of H1 2023 reporting, correspondingly the target for 50% operating profit from capital-light business becomes more difficult to attain.

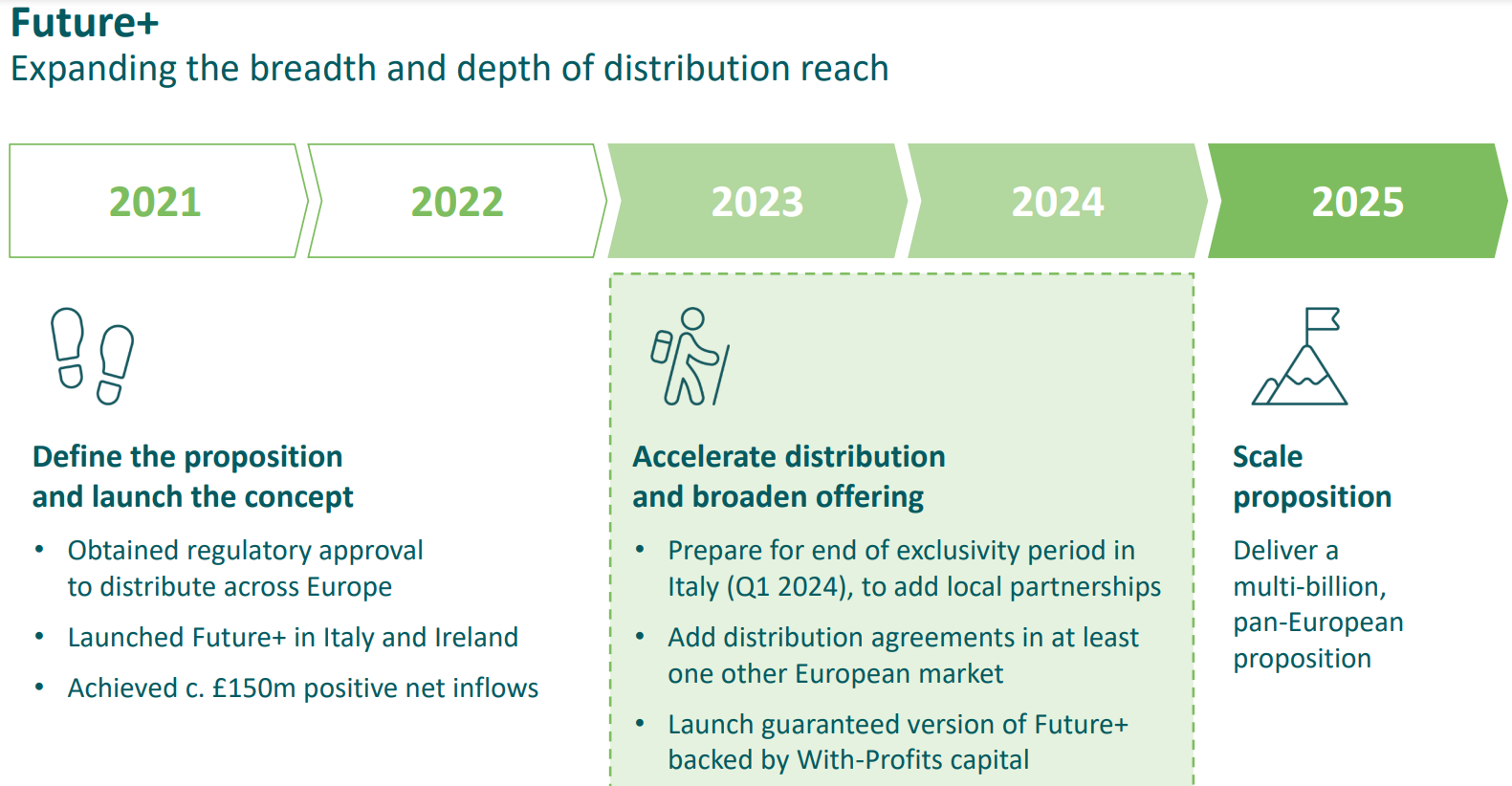

The silent death of Future+

In the preceding steps, I discussed three of M&G’s 2025 targets: the reduction of the leverage ratio to 30%, the capital-light segments providing for 50% of operating income, and the reduction of the cost-income ratio in asset management to 70%. I expressed my reservations about the viability of the latter two goals.

One might object that my reservations are chimeric, that surely an established player like M&G would not lightly give guidance that it doesn’t feel certain about meeting. However, there is one recent example of an exuberant guidance that was given but then, by all appearance, quietly scrapped: Future+ inflows.

Upon presenting the 2022 results, management declared: “We have also made Future+ available to investors in Italy and Ireland. This adds a new growth driver to our international activities. Future+ is a new family of global multi-asset funds delivering smoothed outcomes, designed to replicate the success of our flagship PruFund range outside the UK” (FY 2022 results).

In FY 2022 M&G achieved £150 Mio net inflows to Future+ funds. Mr. Rossi commented on the FY 2022 earnings call: “And I want to say, I mean, I gave the number £150 million and maybe someone would say, well, that is not much. It took us three years in the UK to get to £150 million when we launched PruFund. So in Italy and Ireland, we have done £150 million in one year. So it is actually pretty good.”

But this observation about the decent performance of Future+ in one year completely pales against the projection for fund inflows that is given for the very foreseeable future: “But clearly, we want to achieve, as I said, a multibillion by 2025 on this. And I think we have what it takes” (CEO, FY 2022 earnings call).

The multibillion projection also appears in the FY 2022 presentation:

Evidently there won’t be a sudden jump from £150 Mio net inflows to a multibillion number in 2025 – this is a journey of stages, and here there are really only two stages, 2023 and 2024. Hence, an update at the close of H1 2023 on the progress of Future+ towards the multibillion inflows target would have been appropriate.

However, there was no such update. No mention was made at all of Future+. Not in the earnings report, not in the presentation, not on the earnings call. Even the analysts appeared to have already forgotten about it: no question was asked. I have no explanation for the analysts’ silence, but there is just one for management’s silence: Future+ did disappoint and the mutilbillion inflows target drifted to a more distant future. The projection has been buried.

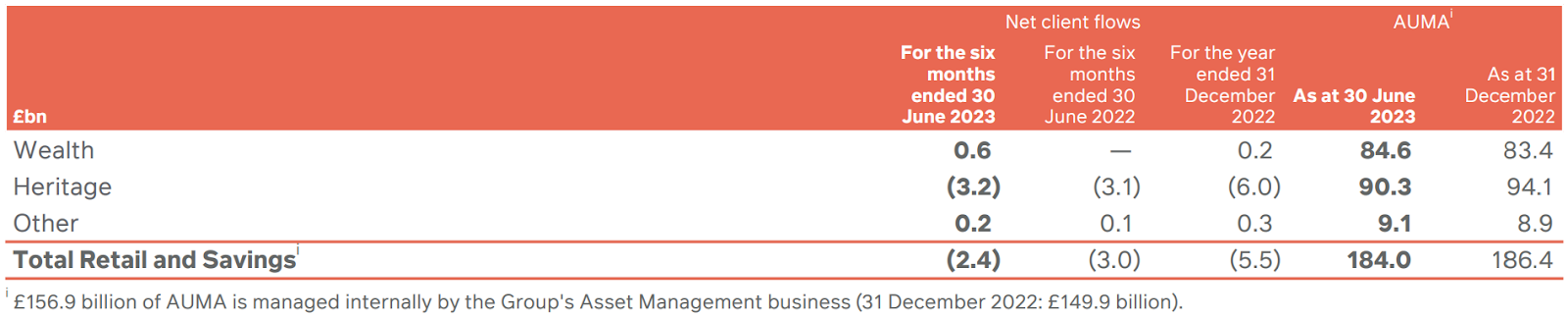

Future+ is grouped with ‘Other’ in ‘Retail and Savings’. Here are the assets under management and administration, and net client flows for Retail and Savings (from the H1 2023 report):

The report explains: “Overall, Retail and Savings (excluding Heritage) achieved net client inflows of £0.8 billion (30 June 2022: £0.1 billion). PruFund is an investment solution offered to clients of both Wealth and Other Retail and Savings. PruFund attracted net client inflows of £1.1 billion for the six months to 30 June 2023 (30 June 2022: £0.1 billion).”

Notably, while ‘Other Retail and Savings’, where Future+ is grouped with, had net inflows of £0.2 billion in H1 2023, the bulk of it might have just gone to PruFund. PruFund, which is spread across ‘Wealth’ and ‘Other Retail and Savings’, had net client inflows of £1.1 billion, but still, Retail and Savings ex Heritage overall only achieved net client inflows of £0.8 billion. This means that, in aggregate, the products in Retail and Savings ex Heritage that are not PruFund had net client outflows of £0.3 billion. While the flows for neither Future+ nor other products are specifically broken down, it can be readily inferred that, if Future+ did not suffer outflows, it was at least very far removed from scaling towards the multibillion pounds inflows that management projected for 2025. Hence, my conclusion is that this guidance can already be called a missed one.

I would have expected management to discuss their former projection for Future+ when presenting the H1 2023 results, to provide reasons for why it was erroneous, and to give insight into how Future+ could still be turned into a successful product, but with a different time frame. However, burying the projection and covering the product with silence does not resonate with an ability of management to learn from mistakes, adjust course and communicate transparently with shareholders about it.

What can be said is that, at least the more global 2025 targets discussed above have been repeated so often that it would be hard for management to just drop them without further mention when they are not reached.

Conclusion

In this article I’ve discussed three of M&G’s 2025 targets and expressed my reservations about two of them. I’ve also shown that M&G in the very recent past has put out an overly ambitious target, and then quietly buried it. However, there is far greater awareness about the central 2025 targets with analysts and shareholders. When two of those targets won’t be reached – and I’d wager that there is a certain likelihood they won’t – it would put M&G’s credibility needlessly on the line if they treated their miss in the same way as the Future+ projection miss: with the silent treatment. The impression that management is prone to putting forth overenthusiastic targets would be less detrimental to credibility than the failure to address the failure to meet those targets. Consequently, it would be conducive to fostering trust with shareholders to address missed targets openly and to guide for a new, more realistic timeframe to meet the same targets. If management misses enthusiastic targets, this might lead to short-term fluctuations in the stock price, but if a constructive post-mortem of missed objectives is undertaken, long-term shareholder trust and appreciation of the capital market would not be impaired.

If M&G fails to eventually meet some of their 2025 targets, which I find some reason to believe, a different communication style than upon the burying of the Future+ 2025 projection would be justified to establish a more honest communication basis with shareholders, and the capital market at large.

M&G is in no rush. They are past the stage of a company that would need to issue equity, nor are they in distress; to the contrary, they’ve bought back shares in 2022. They’re in a different life-cycle, they play a different game. There’s no need for them, no need at all, to massage their stock price with flashy targets. M&G’s heritage dates back to 1848. They can disappoint in the short-term, but it seems evident to me that, as an asset manager, as an insurer, they must be adamant about transparency and integrity to continue playing the long game, this generational game that is and should be part of their culture.