United Mobility Technology: Waving the red flag

United Mobility Technology: Waving the red flag

[All numbers and statements are taken from official company releases on the UMT webpage, www.umt.ag. Statements in German have been translated to English to the best of my ability.]

My original article about UMT can be read here.

In that article I presented what I called a “thought experiment”. It was, despite the cautionary tone, a bull case for UMT. No bull case is any good without a bear case, but I wanted to wait for the full year 2022 results before engaging in writing it. They came out, very belatedly, on the 11th of October 2023. However, in July, upon company news hinting at fundamental deterioration, I attached a warning to the original article, lest anyone should take the thought experiment of the bull case too far.

In the following, again, I present a thought experiment. What I mean by that very clearly is, it’s no investment advice, neither long nor short. Besides that, all assessments and judgements I make are my personal opinion only, and, I reiterate, my personal opinion in a thought experiment that could also have been thought otherwise.

The bear case will be best written by responding to the most bullish statements of the bull case, so I will be doing that here. The quotes from the original, bullish article are in bold. Starting with:

“The company’s third source of revenue is its collaboration and process management software MEXS, acquired in July 2022.”

MEXS doesn’t belong to UMT (yet?).

This actually surprised me. In the HY2022 report, they wrote: “The acquisition of MEXS GmbH took place only after the balance sheet date, so MEXS is not yet taken into account in the current half-year financial statement.” They wrote in the past tense – “took place”, in German, “erfolgte”.

However, in the FY 2022 report we learn that the acquisition actually did not take place: “In July 2022, UMT AG announced its planned acquisition of the MEXS Group, which was subject to the approval of the supervisory board. This approval has not yet been given by the supervisory board.”

But MEXS is not important in the grand scheme of things. It is mentioned here because it is not the only acquisition that turns out really hasn’t been acquired (yet?).

“UMT’s second source of revenue is its smart rental app for equipment for the construction sector: the Buchberger Group, acquired in February 2021. Buchberger Group rents out construction machines via their digital platform connecting them with potential tenants.”

This statement decidedly needs to be changed, and its change has a profound effect. Buchberger maintains that it hasn’t been acquired by UMT. First, it is important to understand that UMT did not acquire Buchberger in cash, but in a transaction that could be best described as an all-shares deal. UMT issued new shares – a capital increase –, and Buchberger was acquired with the UMT shares as currency. However, Buchberger contests the acquisition.

The new CEO of UMT, Erik Nagel, explains in his letter to shareholders: “The main point of dispute is the question of whether the capital increase, which was the basis for the contribution of the shares of the Buchberger companies to UMT AG, was effectively registered with the commercial register in good time. The background to this was to ensure the implementation of the capital increase and the creation of the new shares, because the purchase price for KB Holding GmbH [Buchberger] was to be financed from this. The capital increase was filed in due time, it was entered in the Commercial Register, and the shares were created. However, KB Holding GmbH claims that the registration suffers from formal defects and is therefore invalid."

In my update to the original article, I still wrote: “From a former announcement, I thought the legal case all but resolved; however, even unresolved I believe it’s not consequential.” Here’s what I thought had happened – and Mr. Nagel’s explanation above appears to support that view at least directionally: Buchberger was to receive an X amount of UMT shares and with the stock price at then 8 EUR – roughly – they figured it would add up to 23+ million. But upon the announcement of the deal, shareholders, confused by the pivot of UMT to the old economy, sold en masse, the stock price plunged and Buchberger didn't find the UMT shares so attractive after all, so they searched for a technicality, a minor issue, a detail that went wrong they could take advantage of to call off the deal. Consequently, I thought courts would quickly dismiss Buchberger’s objection. But not so.

On September 12, 2023, The Ingolstadt Regional Court’s 1st Chamber for Commercial Matters rejected UMT AG’s lawsuit claiming ownership of Buchberger. This really was a heavy setback for UMT in their legal dispute. Even so, they announced in the press release: “UMT AG considers the judgment to be grossly unlawful and has already filed an appeal against it with the Munich Higher Regional Court.” Hence, the matter is still not entirely resolved.

Perhaps in appreciation of failing prospects of success in the legal dispute, or really because they want to re-focus on a digital-only strategy, UMT announced in the press release accompanying the FY 2022 report: “As the Buchberger investment does not correspond to UMT AG’s digital brand core, the Management Board has decided to examine exit scenarios for the investment in the two Buchberger companies and the associated legal dispute.”

This declaration is of tremendous importance, I believe, because the FY 2022 results demonstrate that there is no value in UMT other than its stake in Buchberger.

The 2022 half-year results, with which I operated with in writing the original article, contain the Buchberger results, but as Buchberger withheld the financial statements from UMT at that point, the numbers in reality were estimates: “Buchberger Baugeräte Handel GmbH as well as Buchberger Service + Vermietung GmbH have not provided financial data as of June 30, 2022. The inclusion in the interim consolidated financial statements was therefore based on the existing planning and estimates, taking into account relevant information from the relevant markets."

I assumed they were good estimates, but that is besides the point. UMT did not include either estimates or the actual financial statements of Buchberger in the FY 2022 results. While they did include the value of Buchberger in the balance sheet, Buchberger wasn’t accounted for in earnings, revenue, cash flow, or any other metric. And the auditor only put his signature under the report with the following qualification: “The recognition of the investment [in Buchberger] amounting to a total of 15.3 million or 37% of the balance sheet total in the company’s financial statements is currently under question.”

But without Buchberger, UMT has no revenue to speak of, and earnings and cash flow are negative.

This will be shown in the following.

“UMT has shown a strong and resilient performance in the first half of 2022, improving revenue and earnings. UMT has also confirmed its guidance for full year 2022, expecting further growth and profitability.”

But ex-Buchberger, the picture is bleak.

In the six first months of 2022, UMT with Buchberger was reported to have a revenue of 17,54 Mio and earnings of 4,64 Mio. In FY 2022, ex-Buchberger, the UMT AG reported revenue of 0,02 Mio, or, to put it differently, just twenty thousand (!) Euros. EBITDA was a resounding negative 1,33 Mio EUR.

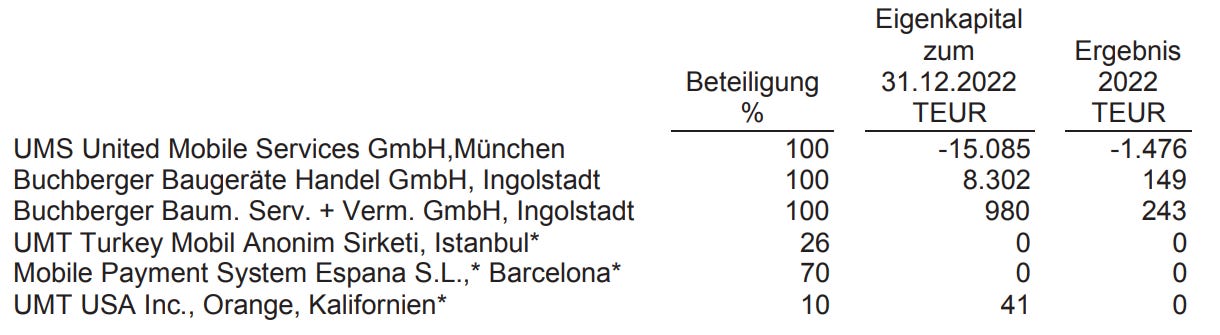

Of course, the UMT AG is not just Buchberger. It is also UMS, and three other, in comparison negligible entities:

The table above, taken from the FY 2022 report, brings us to the next issue, with the next statement in my original article that needs to be scrutinised.

“UMT has a singularly strong balance sheet which supports its growth strategy and financial flexibility.

As of June 30, 2022, UMT had a total capital of EUR 51.2 million, almost unchanged from EUR 50.2 million at the end of 2021. The equity ratio decreased slightly from 97.9% to 95.9% over the same period. In absolute terms, the equity amounted to EUR 49.1 million as of June 30, 2022. The Buchberger group contributed EUR 23.5 million to this amount. A significant part of UMT’s total assets was still the stake in UMS (EUR 9.4 million), which accounted for 18.4% of the balance sheet total, and the receivables from the loan to UMS with 34.1%.”

Where to begin? First, as can be seen in the table above, UMS, UMT’s other major subsidiary (or only one, with Buchberger gone), had negative equity of -15,09 Mio and negative earnings of -1,48 Mio EUR in FY 2022. How are they supposed to ever pay back the loan to UMT? Also, in 2022 this loan slightly increased y/y – again – from 17,13 Mio to 17,24 Mio EUR.

[To be accurate, the precise amount of the loan is not disclosed, though UMT states that the 17,24 Mio of loans to their subsidiaries “essentially” – “im Wesentlichen” – consist of the loan to UMS. Moreover, in the statement about hope being the balance sheet asset, which will be shown further down below, the number 17,24 Mio is given, apparently equating it with the loan to UMS.].

It appears that with this historically growing loan UMT is doing nothing else than shoring up the growing losses of UMS, but still, UMT books this loan as an asset on its balance sheet. The FY 2022 results represent UMT’s equity as the sum of 41.06 Mio EUR. But it needs to be reiterated that of that amount, 17,24 Mio consists “essentially” of an increasing loan to a consistently loss-making company, UMS.

Speaking of which – what is the value of UMS on the balance sheet? And here the successive management teams disagree. On the 5th of July 2023, management under Thomas Teufel declared in a press release: “In addition, the Management Board plans to reduce the valuation of the investment in UMS United Mobile Services GmbH to EUR 0.5 million, as the successes from the payment business have not yet been seen.” This would have been a write-down from 9,4 Mio EUR to 0,5 Mio EUR. All of a sudden, management surprised shareholders with the conclusion that UMS was worth 9 million less than hitherto thought. Losses at UMS kept accumulating – as mentioned above, 1,48 Mio in 2022 alone –, so it appears management decided that they had been waiting too long for UMS to print cash and that is was in reality not worth the value it formerly carried on the balance sheet. Given this write-down of the UMS value, what would the loan to UMS be worth, the 17,24 Mio? Probably next to nothing.

But two weeks after that startling announcement, Thomas Teufel stepped down as CEO of UMT, and Erik Nagel took over. The new management arrived at a different appreciation of UMT in October 2023: “Impairment of UMS GmbH significantly lower than announced in July due to external valuation report”. It is not disclosed who did the external valuation, but it came to a markedly different result than the former internal management, reducing the value of UMS by a comparatively marginal amount to 8,49 Mio EUR. The new management declared: “The announced and unjustified write-down was almost completely reversed, so UMT AG's equity base remains strong and resilient.”

Strong and resilient? On what can the valuation of UMS be based? On its negative equity and the losses it makes? No, it is entirely based on… hope. As states the FY 2022 report: “The future value of the investments in UMS amounting to 8,49 million, as well as the receivables from affiliated companies amounting to 17,24 million, will largely depend on the success of UMS with the solutions it offers in the area of digitalization of processes in business-to-business transactions.”

Hope is an incredible virtue everyone would be blessed to cultivate, but it is hardly an asset on a balance sheet. So UMS and the loan to UMS amount to 25,73 Mio of “assets”. This is 63% of the balance sheet. Hence, 63% of the balance sheet is probably worthless.

Well, what else is there on it? The 15,3 Mio EUR of the value of Buchberger. This was written down from 23,5 Mio, as of last reporting, because of, first, the worsening outlook for the construction industry due to macroeconomic conditions and, second, the ongoing legal dispute. If they lose the dispute, the value of Buchberger, for UMT, vanishes entirely.

However, management even announced to prefer exit scenarios from the Buchberger ownership at this point, as seen above. This is astonishing, because with Buchberger gone, there’s nothing that is left.

Valuation

Somewhere close to zero. Management might perhaps try to manipulate the stock price to keep it above 1 EUR, because then they could issue new shares and thus bring in cash and keep the ship afloat.

Manipulation of the stock price can be done by all sorts of indirect strategies, like press releases promising outcomes that cannot possibly be delivered. But it can also be directly done with purchasing shares of the company on the open market. In the case of UMT, even comparatively small purchases might move the needle. On financial forums it is stipulated, rightly or wrongly so, that Dr. Albert Wahl, the founder and former CEO of UMT, still holds 80%+ of UMT shares with no intention of selling. If true, this considerably reduces the real free float and makes the stock price more susceptible to sudden volume moves.

And here is what UMT did in 2022: they bought 160.820 of their own shares for 693.419,88 EUR and sold all of them but 10 for 664.489,81 EUR, locking in a loss of 28.930,07 EUR on that trade. With a company that has just 20.000 EUR in revenue and a negative cash flow of minus 0,566 Mio EUR, this seems a dangerous game to play. The explanation by UMT of why they sold the shares is questionable: “The proceeds were used to invest in ongoing projects and strengthen the equity base.” I can’t see how selling your own shares at a loss strengthens the equity base; evidently, the reverse is true.

[Update: UMT has been pursuing the buying and selling of their own shares in the first half of 2023 as well, as clearly states the HY2023 report. Again, at a loss.]

This brings me to the tentative conclusion that management sees the only possibility for stock price appreciation in speculation. I’d locate the fundamental value of UMT, ex-Buchberger, somewhere close to zero, but with a thin free float, one never knows what trading could do to the stock price, and I presume management is banking on that to try keeping the stock price above the 1 EUR threshold that allows for issuing new shares and bringing fresh capital in – because in the case of Buchberger gone, how else could cash come in?