Harrow, Inc.: Blurry vision

[The shareholder letters and earnings reports can be found on Harrow’s website: www.harrow.com The transcripts of the earnings calls are provided by various financial services.]

“I do my best to offer transparency, knowing that credibility is crucial to a long-term relationship between Harrow and its stockholders. The value of increasing one’s credibility to stockholders is exponential – on the positive side as it grows, but in turn, it’s incredibly hard to regain credibility and can be increasingly exponentially negative as it is lost” (Q1 shareholder letter).

Those were the words of Mark Baum, CEO of Harrow Inc., in presenting the earnings for the first quarter of 2023 in a letter to shareholders.

Harrow Inc. produces and distributes drugs for the medical eye-care industry in the United States. Its customers principally are ophthalmologists and optometrists.

Harrow has been a revenue growth story on the come in the stock market for the past two years. To a great extent the appreciation of the stock price could be attributed to the integrity and long-term vision that management represented for investors.

But with the release of Q3 2023 earnings on November 13th, the stock price plunged. Shareholders suddenly either found management’s integrity not as spotless as formerly believed, or management’s vision of their future business success blurred.

On one thing we can all have clear vision, though: this blog post is no investment advice, neither long nor short, but written for entertainment purposes only.

Having made my inquiries into the causes behind the sell-off of Harrow’s stock, in the following I discuss what I consider most meaningful for calling the bullish thesis for Harrow into question.

Let’s start with the first concern, inflated accounts receivable, although the argument around it is the most cautious, the most hypothetical of all in this blog post.

1) Ballooning accounts receivable (or: Revenues without cash as far as the eye can see)

‘Accounts receivable’ refers to the outstanding invoices a company has: it is the amount of money owed to a company by its customers. While accounts receivable are already booked as revenue, naturally they only translate into cash flow upon being paid by the customers.

At the end of Q1 of this year, accounts receivable rose to $5,882,000. Harrow explains that the increase was “related to payment terms for the profit transfer associated with the Fab 5 Acquisition” (Q1 report).

For context: Harrow acquired five drugs from Novartis and christened them the Fab 5 (yes, like the drugs were superheroes). But, for some time Novartis kept selling those drugs and transferred the profits to Harrow, before Harrow started selling them on their own. From the statement above I understand that the payment terms for the profit transfer were such that more profits would be transferred later on, which now, momentarily, were only booked as accounts receivable. In essence, Novartis hadn’t been paying Harrow yet all the profits they made from selling the Fab 5, which technically already belonged to Harrow.

In Q2, accounts receivable made a huge leap to $12,038,000. Harrow mainly attributed this to “payment terms for the profit transfer associated with the Fab 5 Acquisition and branded product sales” (Q2 report).

Here we have the same explanation as above, but also the addition of extended payment terms for branded products which Harrow was already selling on its own. Harrow sent out its products, billed for them, and booked revenue for them, but had given its customers the ‘buy now–pay later’ option and thus hadn’t seen the cash for those sales yet.

In Q3, accounts receivable still ticked up slightly, to $12,287,000, which was “related to payment terms for our branded product sales during the nine months ended September 30” (Q3 report).

Strangely, here no mention is made any more of the payment terms of the profit transfer by Novartis. This makes me wonder whether in Q3 Novartis settled all the outstanding accounts receivable related to the Fab 5 acquisition. If so, the $12 Mio accounts receivable at the end of Q3 were entirely attributable to how Harrow sold its own products, that is, with extended payment terms (buy now – pay much later). Or was the $12 Mio made up partly of accounts receivable Novartis still hadn’t settled yet, and partly of Harrow granting extended payment terms in selling the branded products on its own?

Your guess is as good as mine. In any case, those inflated accounts receivable create a lot of opacity one would joyfully dispense of in analysing an already complicated revenue-growth story that has suffered a hiccup.

I want to explain further this opacity I’m talking about. What is the issue with accounts receivable inflating? What could that possibly, conceivably, hint at?

At Harrow, revenue from Q2 to Q3 increased by an anemic 2%, and the market heavily punished that by driving down the stock price. Given this, it would have been downright disastrous for investors’ perception of Harrow’s future success to present, instead of this paltry revenue increase Q/Q, a revenue decline. Generally speaking, Harrow’s story is a revenue growth story and falters when they can’t continue writing that story.

In theory, a company could continue to increase its accounts receivable and report increasing revenues each quarter without ever receiving the cash for the sales. However, in practice, this would violate the revenue recognition principle, which states that revenue should only be recognised when it’s realisable.

Companies could issue fictitious bills that overstate the amount due from customers, leading to an apparent increase in revenues. Once a bill is sent out and the revenue is recognised, maybe after that the payment is never received and will have to be written off. Even so, the advantages resulting from an unreal revenue increase persist. The perceived increase benefits all stakeholders in the company: management meets revenue targets and the stock price levitates, painting a smile on shareholders’ faces.

Harrow, however, makes allowances for account receivables it expects it won’t be able to collect:

In this case, the company has an allowance for credit losses of $108,000 so far for this year. This means that out of the total accounts receivable of $18,468,000, Harrow expects that it won't be able to collect $108,000. Which still leaves $18,360,000 to be collected in the future.

But it’s also conceivable, at least conceivable, that a company tinkers with their allowances. For instance, it could write off uncollectible accounts without flagging them as bad debt and instead hide them in another accounting item, with ‘Selling, General & Administrative (SG&A) expenses’ being a suitable candidate. There the uncollectable customer debt could be written off invisible for shareholders as a general SG&A expense. Shareholders might mistakenly believe that the increase in the SG&A expenses item was due to an expansion of the sales force or other operational growth, rather than an increase in bad debts.

I insist that this is just a theoretical thought experiment about what could happen. It doesn’t correspond to the actual data Harrow reports. Admittedly, SG&A expenses jumped from $15.9 million in Q1 2023 to $20.0 million in Q2, and further slightly increased to $21.0 million in Q3. However, this increase can be convincingly explained by the very reasons that management gives for it, that is, “an expansion of our general operating and sales infrastructure to support our branded product acquisitions and launches in 2023, coupled with an increase in stock-based compensation of over $3 million largely associated with management performance stock units” (Q2 stockholder letter).

Still, for the time to come, if the accounts receivable number doesn’t fall substantially but instead continues rising, shareholders should match it with the rise in SG&A expenses and other items in which written-off receivables could be buried invisibly, and shareholders should scrutinise management’s explanations for why those accounting items rose.

Finally, inflated account receivables might be an indication of the practice of overloading the supply chain, also called ‘channel stuffing’.

In the case of Harrow, if any of the scenarios presented here is true, I estimate this to be the most likely.

In overloading the supply chain a company delivers more products to its distributors than the end-consumers (here, the patients) are expected to consume in a standard inventory cycle. To convince distributors to acquire more than their immediate requirements, they are offered significant price reductions, refunds, and extended payment periods. Overloading the supply chain leads to a sudden increase in accounts receivable. It can inflate revenue figures for some months, as it heavily frontloads future transactions.

The accounts receivable were also mentioned by an analyst, Mr. O’Neil from Lake Street Capital Markets, on the Q3 earnings call. I don’t quite think the answer by Harrow’s CFO, Mr. Boll, puts the question to rest: “On the cash flow side, and more so just talking about AR [accounts receivable] in particular, because we introduced these branded products, we have a different type of AR and receivables cycle than we have seen on the compounding side. And on the IHEEZO, in particular, for our customers buying IHEEZO, we've been able to extend them additional terms, and that just helps them with their revenue cycle and cash management cycle. For us, what that means is our collections on the branded side are a little bit lengthened out compared to other companies we have historically seen.”

While Mr. Boll’s statement can’t be taken to be indicative of the practice of channel stuffing, admittedly it also doesn’t exclude that such a practice has been resorted to, to momentarily boost IHEEZO sales and present at least some growth in overall company revenue from Q2 to Q3.

Mr Boll continues: “ … I'm seeing over $16 million in AR on the branded side that we should be able to collect this quarter, and then that will be in addition to the AR and cash receipts we're receiving on the compounding business. And so I think we've gotten through this sort of initial term around the launch with IHEEZO and these branded products, and we should start seeing sort of the AR with the branded products turn a little bit more, more cash receipts coming in and less of a larger spread on AR compared to revenue going forward.”

Here Mr. Boll makes a very important statement which will be easily verifiable with the Q4 accounts receivable number! I repeat and insist: it will be verifiable, and all eyes should turn to that number once the Q4 report comes out next year. If accounts receivable don’t drop down substantially, as Mr. Boll affirms they will, it will cast further doubt either on management’s ability to assess the progress of their business, or on their honesty vis-à-vis their shareholders.

2) Debt (or: Imagine you’re really deep in the red. Real deep.)

Is debt an issue? Without a doubt, it is, by just appreciating the sheer amount of it:

The amount, though, is less important than the interest rate at which this debt is serviced: “For the three and nine months ended September 30, 2023, the total effective interest rate of the Company’s debt was 10.78%, and 10.91%, respectively” (Q3 report).

The interest to be paid on the debt translates into the following yearly expenses going forward:

I assume debt repayments that come due in 2026 and 2027 won’t be able to be met, but will be refinanced under practically the same terms and conditions. With that, Harrow should be expected to ultimately pay roughly the same for debt servicing as in the two years prior, 2024 and 2025.

Debt servicing is, however, not the only financial obligation Harrow needs to take into account. It also has to pay lease on company facilities. The payments to be expected for those are presented here:

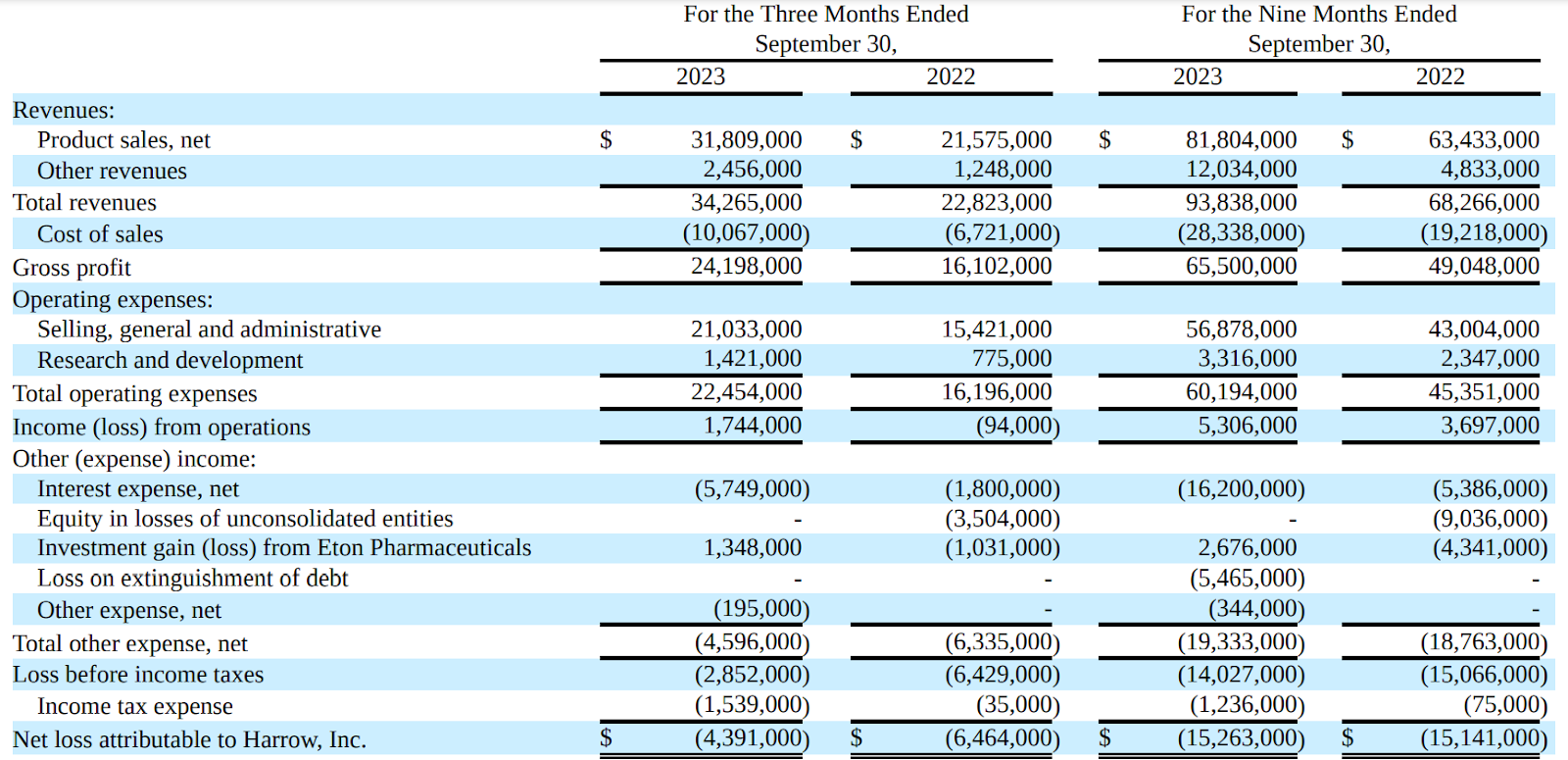

To assess whether Harrow will likely be able to meet its financial obligations, I’ll take into account their income statement, their cash flow statement, and management’s revenue outlook. First, here’s the latest income statement:

As can be seen, the interest expense paid on its debt alone eats away Harrow’s income from operations multiple times, resulting in a significant loss in the bottom line.

As to the prospects of top-line growth: While the table above shows a marked increase in sales from 2022 to 2023, sales from Q2 to Q3 2023 actually slowed substantially, just rising by 2%, as has been mentioned before.

I think the base case should always be the worst case, and for this reason, I shall not assume any sales growth with the current drug portfolio from Q3 2023 onwards. Correspondingly, ‘cost of sales’ and ‘operating expenses’ should stay the same.

In making this assumption I imply another one. Harrow doesn’t sell yet one of the Fab 5 drugs, TRIESENCE, and plans to commercialise it some time in 2024. With TRIESENCE commercialising, very likely further debt of $35 Mio will come rolling in: “Following entry into the Oaktree Amendment and the funding of the Loan Increase upon closing of the Santen Products Acquisition, the Company has drawn down a total principal loan amount of $77,500,000 under the Oaktree Loan and an additional principal loan amount of up to $35,000,000 remains available to the Company upon the commercialization of TRIESENCE” (Q3 report). Interest expense on the $35 Mio, with the rate at roughly 10%, would be $3.5 Mio per year. I assume here that whatever Harrow will be able to make annually from the commercialisation of TRIESENCE will suffice to cover those additional interest costs, but won’t increase the income from operations for the company.

Obviously, following the above assumptions, Harrow would incur a net loss of roughly $18 Mio for entire 2024 (4.4x4=17.6), and again for 2025, and so forth. But what does this actually mean in terms of cash loss?

The cash flow statement clarifies this:

With having bled some $5 Mio of cash in operations in the first nine months of 2023, this translates into a cash-bleed run-rate of $5 Mio/9 months = $0.555… Mio/month x 12 months = $6.7 Mio per year. At the end of Q3, they held total cash of $65,610,000. In other words, continuing a cash burn of roughly $7 Mio per year, they can last for nine years before the lights go out.

[I do not take into account here the possibility of them raising capital by issuing equity again. Sadly for the diluted investors, they haven't shied away from doing it as late as this year.]

But how low can they go in cash without breaking the debt covenant with Oaktree, their lender? “Minimum Liquidity Amount” means $15,000,000 … the Obligors shall at all times maintain the Minimum Liquidity Amount in cash and/or Permitted Cash Equivalent Investments” (Q3 report).

So not to trigger possibly substantive adverse events for the company, in reality they can only continue their current rate of cash burn down to $15 Mio, that is: for seven years. They have seven years to continue dragging along with the nigh-stagnant revenue growth seen from Q2 to Q3 2023, but after that, cash flow from operations must rise by at least seven million per year to not breach the debt covenant with Oaktree.

Now, let’s take a look at what Harrow guided for in 2024: at least $180 Mio in revenue. Given that from Q2 to Q3 they had to reduce their revenue guidance for full year 2023 from $139 Mio midpoint to $133 midpoint, they apparently don’t have good visibility on even the very near-term success of their business (more on that below). For this reason, I would assume that their longer-term visibility is even more impaired. So I’d rather calculate with flat revenue from 2023 to 2024. As to expenses, they’ve guided for 2024 as follows:

“From a cost structure perspective, we expect our operating costs to increase incrementally as we scale our business to grow revenues and invest in the VEVYE launch” (Q3 shareholder letter).

I assume here that VEVYE falls in every way short of its promises and that the only revenue it brings in is such as to cover the expenses deployed in its launch and ramp-up, and I likewise assume that all further operating costs incurred to drive up the revenue of the other products will only drive up revenue so much as to cover the additional operating costs.

Hence, all things stay equal and Harrow’s life span before breaching the minimum cash debt covenant with Oaktree is seven years.

Why am I doing this grim napkin calculation at all?

I commonly do it when a company runs into problems that historically has shown the ability, under current management, to figure its problems out and move forward. And Harrow has historically shown no lack of figuring things out.

Reflecting on their past history of growth, Mr. Baum reminded shareholders in his Q4 2022 letter of the company’s steep rise from 2018 to 2022:

“• Annual revenues increased 232% from $26.7 million to $88.6 million, a 35% CAGR.

• Core gross margins increased 47% from 49.6% to 72.9%.”

Obviously past performance gives no insight into future performance, but it’s still the only way to assess the viability of projections about future performance. Harrow has historically overcome problems, and if we might extrapolate that, they will eventually overcome their present growth problem – all things being and remaining equal, they have seven years to figure it out before running into substantial trouble. This should be more than enough time for them to come up with solutions.

That’s how I see it. And even though, as mentioned, I believe the base case with which I operate here is actually the worst case, I have an encroaching doubt that perhaps I’m still being too optimistic. Where does this doubt come from? It’s one part of Harrow’s 2024 guidance that kindles this suspicion in me:

“We remain confident in meeting our obligations to Harrow’s creditors.”

My base case doesn’t envision the slightest concern that Harrow will be able to meet its obligations to creditors in 2024. For this reason, I’m very surprised by management including this explicitly in their 2024 guidance. It makes me wonder: if you run a company and don’t have the shadow of a doubt that you will be able to meet obligations to creditors, it would be such a non-issue to you you wouldn’t think about giving guidance on that. Nor would shareholders think you’d need to. Because companies that do give guidance about being able to pay interest on debt in the year to come, are usually companies in financial distress whose shareholders want management to give some assurance about their ability to service debt in the year to come. Is such the case for Harrow?

Moreover, the wording of this assurance, “we remain confident”, does not exactly inspire confidence. Assuming my base case is correct – which, again, to my understanding is the worst case – then management would rather be expected to say: ‘We are absolutely convinced that we will meet our obligations to Harrow’s creditors.’ So I’m wondering whether I’m missing something and whether my base case is more optimistic than I should allow it to be.

Either this, or Harrow is just generally bad about giving guidance on anything.

3) Guidance to nowhere

Before Harrow’s stock price deflated considerably, it had been inflated by management’s high hopes about the future which they expressed with a lofty revenue guidance for five years hence:

“‘What are the ‘highest financial goals’ of our Five-Year Strategic Plan?’ Simply put, we believe that – with our current product portfolio and continued strategic execution by the Harrow team – we can become a top-tier U.S.-focused ophthalmic pharmaceutical company capable of producing annual revenues of $1 billion or more – at very attractive operating margins” (Q2 shareholder letter).

An annual $1 billion revenue run-rate by the end of 2027. That guidance was quite the whopper. But the whopper didn’t have long legs, it appears. Already three months later management had to admit that they were behind the plan: “Today, we find ourselves a few months behind our internal development timelines for some of our programs” (Q3 earnings call).

A few months. This is noteworthy. What is a few months? Evidently at least two, but more probably three. And for the company as a whole, management states, in reference to their 5 year plan: “the aggregate progress of our business is about 60 days behind” (Q3 shareholder letter).

So three months after giving out their $1 billion guidance management admits they find themselves at least two months behind fulfilling that guidance. If now you believe that makes little sense, then yes, you’re right.

One naturally presupposes that, when a company gives out guidance for what their revenue will be in five years, they have some solid internal plan to arrive at that revenue target. But Harrow, almost immediately after conceiving their five year plan, came out saying they couldn’t make it as conceived. One might argue that this shows management’s inability to dress up a five year business plan. At least it’s difficult to argue for what else it could mean, other than misleading shareholders.

It gets even better (I mean, worse). The five year plan of course consists of steps, and each year is a step.

On the 9th of August, almost half-way through Q3, management in their Q2 shareholder letter asserted the 2023 full-year guidance: “Recognizing that our Five-Year Strategic Plan consists of a series of One-Year Plans, based on our results to date, we remain confident in our 2023 financial guidance of $135 million to $143 million in net revenues and $44 million to $50 million in adjusted EBITDA. Regarding our 2023 financial guidance, we intend to provide an update to our financial guidance later in the year after we have a few months of operations under our belt with our new product portfolio” (Q2 shareholder letter). Specifically, they declared: “Related to this point, our 2023 financial guidance was conservative and did not include much IHEEZO revenue” (ibid.).

Both the Q2 shareholder letter and the corresponding earnings call were exceptionally upbeat about Harrow’s immediate and long-term prospects, and the 2023 guidance was flagged as ‘conservative’. What else could the inclined shareholder believe upon reading the statements above, but that Harrow would revise guidance upwards when updating later in the year?

But not so! Not so. Instead, upon presenting the Q3 results, they revised downwards:

“Because the aggregate progress of our business is about 60 days behind, we are adjusting our 2023 revenue guidance from a range of $135 million to $143 million to a range of $129 million to $136 million” (Q3 shareholder letter).

Let’s contemplate this fact for a moment. Is it imaginable that on the 9th of August, half-way through Q3, management had no idea that Q3 results would ultimately force them to revise guidance downwards? If this were true, if they had no idea, it would shockingly demonstrate that management has no near-term visibility on the success of their business. Of course, this would also completely belie any long-term visibility they claim to have. But instead let’s suppose that management half-way through Q3 knew that things weren’t going according to plan and just decided to hide it from shareholders. Then this would substantially impair the value of credibility stock market participants have attributed to Harrow’s management so far.

Either conclusion casts doubt on management’s ability to direct a public company and is thus damaging to any investment thesis for Harrow one might come up with.

In the Q2 shareholder letter, Mr. Baum wrote: “As Harrow’s CEO, credibility is my primary currency.”

You can come to your own conclusion about the worth of that currency since the Q3 earnings report.

4) IHEEZO in-office (or: The risk that hits you out of nowhere)

IHEEZO is an anesthetic for cataract surgeries and other procedures requiring the anesthesia of the ocular surface.

Before I reproduce the risk statement regarding IHEEZO contained in the Q3 report, I want to highlight that it came completely from left field out of the blue.

IHEEZO is used both in hospitals and in-office settings, and the latter are of paramount importance to IHEEZO becoming the success management wishes it to be. “We estimate that the number of use cases for the physician’s office setting of care is double that of the ASC/hospital, creating a multi-billion-dollar annual revenue opportunity for IHEEZO. Therefore, the physician’s office setting of care is our primary market for IHEEZO, and the ASC and hospital market is secondary” (Q2 shareholder letter).

IHEEZO was said to have a permanent J-Code for the office setting, which means that doctors using it in the office get reimbursed for the product by Medicare.

“And so we're really pleased now that the doctors who are using it, we're seeing them get reimbursed not only in the ASC setting of care the hospital study of care, but also in the for the in-office setting of care. … And as I said, I think the big picture message with IHEEZO is that last piece of the puzzle to ensure adoption of the product. When you have a product that works like IHEEZO you want to make sure and it does have a J-code, which IHEEZO has, we want to make sure that physicians are able to build the code. And that was the last piece of the puzzle and we're seeing the code get paid. And so there are really no barriers to doctors now adopting the product. And that's I think very, very positive” (Q2 earnings call).

So here it is. Doctors in-office have been briefed on how to ‘build’ the J-Code and they are getting reimbursed for IHEEZO. With that, the last lingering issue, the last barrier has been overcome, because now, now there are no barriers left for doctors to adopt IHEEZO.

Well, not quite.

Suddenly, in Q3, a new issue has come up. So momentous apparently that management had to include it in the “Risks” section of the Q3 report. It relates to CMS’s billing policy. CMS, the Centers for Medicare & Medicaid Services, is the federal agency that administers the nation’s major healthcare programs, including Medicare. I reproduce the risk statement regarding IHEEZO here in full:

"Relatedly, despite IHEEZO being issued a J-Code for physician-office billing, CMS has an existing policy on anesthesia billing which has historically not allowed for the separate billing of anesthesia services in the physician’s office, which could be viewed in conflict with IHEEZO’s reimbursement status for in-office applications. Because our application for a J-Code for IHEEZO specifically disclosed the likely significant utilization of IHEEZO in the physician’s office setting of care, along with additional communications to this effect, we intend to request that CMS clarify that J-Code 2403, IHEEZO’s permanent J-Code is appropriate to be billed for the anesthesia itself (i.e., IHEEZO in our case) in the physician’s office setting. If CMS disagrees with our position, it is possible the separate reimbursement of IHEEZO would be limited to the surgical setting only (e.g., ASCs [hospital setting; my addition])."

What is said here is, if CMS doesn't agree with Harrow’s view, doctors in-office might either bill for the anesthesia/drug itself (that is, IHEEZO) or for the service of providing anesthesia, but not for both. What this entails, concretely, I believe has been poorly explained by management in the shareholder letter, which in essence only repeats the information given in the risk statement. But we might conclude that, if CMS disagrees with Harrow, the enticement for doctors to use IHEEZO in-office will be lower, because they will be either reimbursed for IHEEZO or for the service of them administering IHEEZO, but not for both. Management hasn’t disclosed which impact on their expected revenue from IHEEZO the possibility of CMS not agreeing with them would have. Some impact it must have, evidently, because else there would have been no need to include this issue in the risks section.

The shareholders are left in the dark about the possible adverse revenue impact of that risk.

5) IHEEZO’s October performance (or: The imperfect chart crime)

The commercial development of IHEEZO is crucial for the Harrow story, as Mr. Baum underscored on the Q2 earnings call: “I believe IHEEZO and VEVYE are our largest revenue opportunities without question.” [IHEEZO has been launched in 2023, and VEVYE hasn’t been launched yet.]

Management is all too aware of shareholders being aware of IHEEZO currently being the principal driver of the Harrow story, so much aware indeed that management appears to represent the sales data in a biased way which might paint a rosier picture than reality. They print the following chart in the Q3 shareholder letter:

The choice of the data points – 14 April, 12 May, 4 August and 27 October – is puzzling, and indeed no reason is given for their use. What stands out, however, is that no data point for September is shown. It stands out because management has to say the following: “IHEEZO unit volumes and revenues ramped significantly during September” (Q3 shareholder letter). If purchases, after ticking up dramatically in September, flatlined or slightly fell in October, one would be unable to tell so from that chart, because for each data point it shows the average customer unit demand for the twelve preceding weeks. Indeed, Bloomberg data shows flatlining sales from September to October – because it was the same number, some shareholders interpreted this as a data artifact. But actually, with management not showing a data point for September in the chart, this rather suggests that the Bloomberg data was correct: with a data point for September missing, management can make it appear as though purchases of IHEEZO continued rising in October.

Hence, assuming the Bloomberg data is correct, the chart is grossly misleading.

Moreover, it shows units purchased, which might imply that the units purchased could simply have been driven up by (heavy) discounting of the product and therefore not correlate to a similar ramp-up in revenue.

On the Q3 earnings call, Mr. O’Neil enquired about the strategic shift that enabled Harrow to ramp up IHEEZO significantly in September, but management did not give a direct answer: “We did make some strategic amendments to the strategy, the launch strategy in late August, and things kind of were implemented by September. I can't go into the specific tactical details of our strategy really to our stockholders, but also to potential competitors. I think the important thing is that we did. In fact, see this major ramp when we made these changes, and that's important. I know I spoke to a lot of stockholders after the last earnings call, and they wanted to see some numbers that were accurate and so we provided them. And all I can tell you is that we not only provided numbers that, I think validate the success of the changes that we made, but importantly, we provided numbers that get us into the fourth quarter. So we've seen a continuation of that ramp, and we don't expect that to yield.”

There are some things in this answer that need highlighting. First, management didn’t provide accurate numbers with their chart, as has been argued above, albeit Mr. Baum’s assertion that they did; second, the numbers do not validate the success of the strategic shift, as they only show unit demand, but not revenue; third, the numbers don’t get us into the fourth quarter, as they provide the average of the past twelve weeks for each data point, and a data point for September is missing.

Speaking of the fourth quarter, on the earnings call Mr. Baum further mentioned that: “We are now seeing sizable orders and reorders from high-volume users and many new accounts, both large and small, who are enjoying the many benefits of IHEEZO” – but this might only mean that October sales for Iheezo were as good as September sales, nothing more.

If sales of IHEEZO did not increase sequentially from September to October, as the Bloomberg data indicates, shareholders, who are explicitly called partners by Mr. Baum, would have deserved to know that truth.

Summary

Let’s sum up.

We have high albeit for at least the next seven years manageable debt (I daresay), curious revenue guidance missed either by inability to forecast or by shortcomings in honesty, an intransparent risk to the revenue bonanza IHEEZO in-office sales are meant to provide, a misrepresentation of the demand for IHEEZO from September to October, and ballooned accounts receivable that limit the view-through to net revenues providing real cash flows. And this unfavourable mix is permeated by anemic revenue growth from Q2 to Q3 2023.

These are not the only issues, but the ones I deem most important. Others might consider other issues more important still. However that may be, one thing is clear: there is no shortage of issues.

It’s more than understandable that shareholders weren’t convinced upon the presentation of the Q3 earnings and sold off the Harrow stock en masse.

To return to the quote given at the beginning of this blog post, Mark Baum, Harrow’s CEO, described succinctly six months ago what has been happening to Harrow’s stock now:

“it’s incredibly hard to regain credibility and can be increasingly exponentially negative as it is lost” (Q1 shareholder letter).

How hard it will be, the next quarters shall show.

Thank you for explaining how a company might hide credit losses. Regardless of whether this happened at Harrow (and it seems it wasn’t the case based on the recent stock price surge), this helps me better understand income statements.